Understanding where your money beliefs come from, and how to revise them

Understanding where your money beliefs come from, and how to revise them

Understanding the money beliefs social workers develop helps explain why many professionals struggle with financial wellbeing even when their income improves.

In my previous article, Financial Stress Social Workers Face: Why Low Pay Isn’t the Whole Story, I explored why financial stress in social work goes deeper than low salaries.

Today, I want to show you WHERE the money beliefs social workers develop, and how to revise them using insights from financial social work.

Because understanding your relationship with money isn’t just about feeling better about finances. It’s about changing the actual behaviors that determine your financial circumstances. These beliefs are often called money scripts in financial social work research.

Quick Answer: Your Money Story and Financial Beliefs as a Social Worker

Your relationship with money was largely formed in childhood through family financial socialization and then reinforced by social work training that valorizes self-sacrifice. These unconscious money beliefs, what researchers call “money scripts,” directly shape your financial behavior: how you earn, spend, save, and invest. And your financial behavior determines your actual financial circumstances.

5 Common Money Beliefs Social Workers Develop

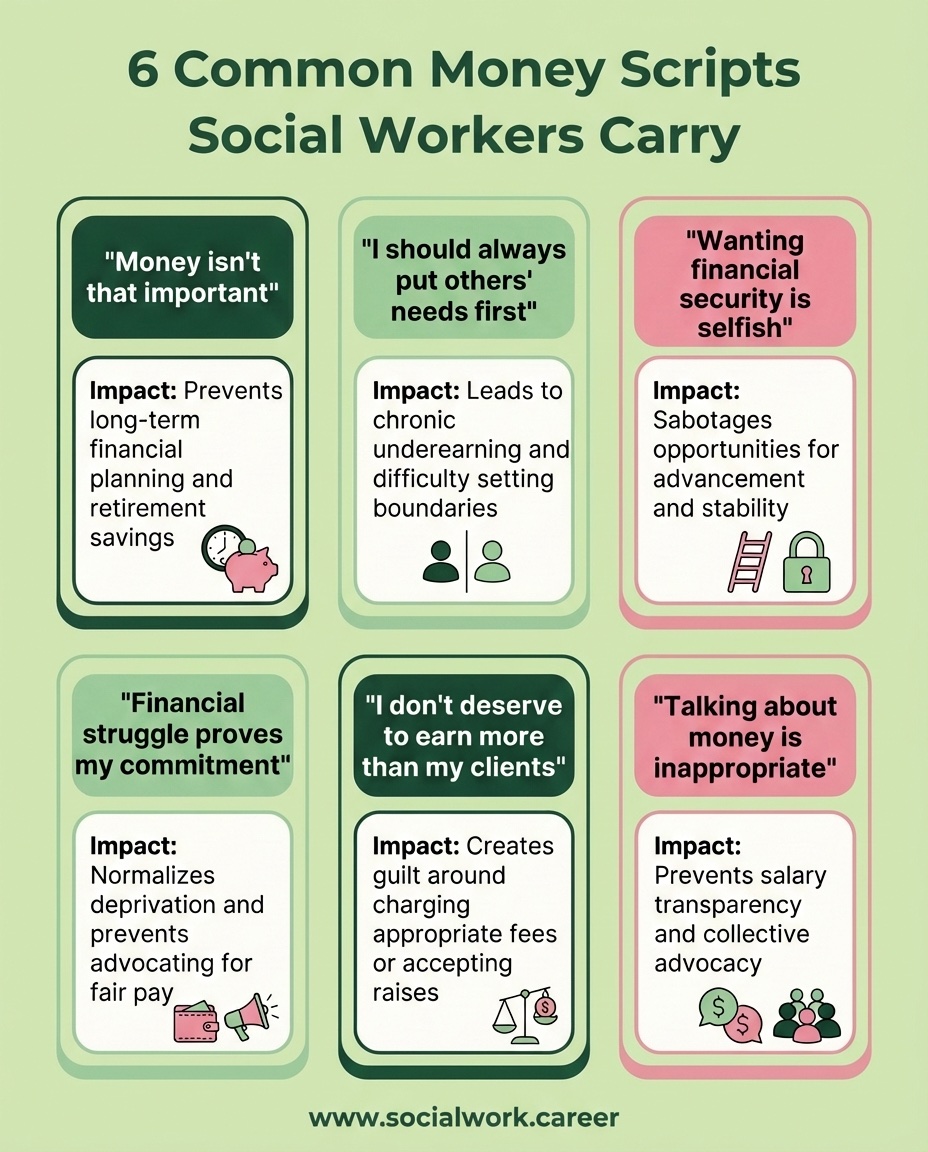

- “I should always put others’ needs first” – Leads to chronic under-earning, difficulty negotiating, and guilt around spending on yourself.

- “Money isn’t that important” – Prevents building savings, planning ahead, or advocating for fair compensation.

- “Wanting financial security makes me selfish” – Sabotages negotiating, saving, or investing as acts of self-care.

- “Financial struggle proves my commitment” – Keeps you in underpaying roles and frames hardship as virtue.

- “I don’t deserve ease” – Unconsciously recreates financial stress even when circumstances improve.

Why Understanding Your Money Story Isn’t Enough on Its Own

Insight alone rarely changes financial behavior. Money scripts are stored in the nervous system, not just the intellect, which is why knowing where a belief came from doesn’t automatically make it stop running. Revising your money story requires both understanding the belief and addressing the emotional and somatic patterns underneath it. This is the foundation of Financial Social Work, the interactive behavioral model developed by Reeta Wolfsohn, CMSW, founder of the Center for Financial Social Work, which helps people explore and shift their unconscious feelings, thoughts, and attitudes about money at a deeper level than budgeting or financial planning can reach.

Research Finding: Money scripts are absorbed before age 7 and continue to shape adult financial decisions (Klontz et al., 2011). These are the money beliefs social workers absorb before they even have language to question them. For social workers, these childhood beliefs are compounded by professional socialization that valorizes financial sacrifice, creating layered patterns that work against financial wellbeing at every level of the Relationship, Behavior, Circumstances chain.

Your money story isn’t a character flaw. It’s a set of beliefs formed before you had the language to question them, and it can be revised. But revision requires both personal work and an honest look at the systemic conditions that make financial wellbeing harder for social workers to build.

HOW THIS SHOWS UP IN YOUR FINANCIAL LIFE

The psychological patterns we explored in the last post don’t just live in your head; they directly shape your financial behaviors and, ultimately, your financial wellbeing.

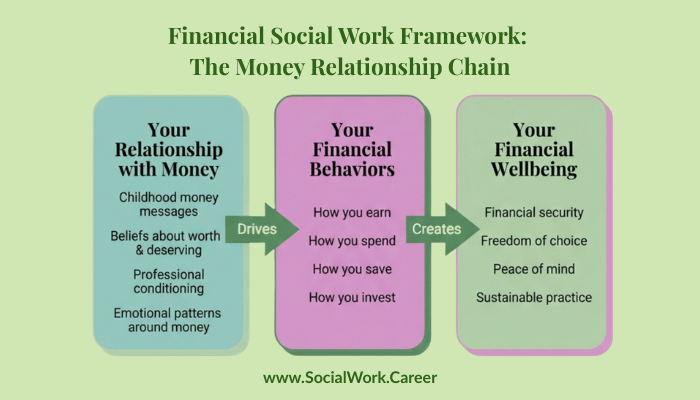

This is where financial social work offers crucial insight: your relationship with money drives your financial behavior (how you earn, spend, save, and invest), and your financial behavior determines your financial circumstances (Wolfsohn & Michaeli, 2014; Sherraden & Huang, 2019).

The Relationship → Behavior → Circumstances Chain

For social workers, this chain often looks like:

- Earning: Not negotiating salaries, undercharging for private practice services, avoiding higher-paying leadership positions because they feel “less mission-driven”

- Spending: Difficulty spending on yourself without guilt, or conversely, overspending on others to prove you’re “generous” or “selfless”

- Saving: Inability to build emergency funds (unconsciously sabotaging stability), or avoiding saving entirely because “there’s never enough anyway”

- Investing: Avoiding investing altogether because it feels “corporate” or incompatible with helper identity, missing out on long-term wealth building

These aren’t random habits; they’re behavioral expressions of the money messages you internalized growing up and throughout your social work training.

The psychological patterns we explore in the last post don’t just live in your head; they directly shape your financial behaviors and, ultimately, your financial wellbeing.

This is where financial social work offers crucial insight: your relationship with money drives your financial behavior (how you earn, spend, save, and invest), and your financial behavior determines your financial circumstances (Wolfsohn & Michaeli, 2014; Sherraden & Huang, 2019).

These financial behaviors don’t exist in isolation. They are often shaped by broader financial pressures in the profession.

In my previous post on financial stress social workers face, I explored the financial stress social workers experience and why it isn’t only about low pay. Financial stress often reflects a deeper relationship with money shaped by childhood experiences, professional conditioning around self-sacrifice, and repeated exposure to clients’ financial crises.

To understand where those patterns begin, we have to look earlier, at the money messages we absorbed growing up.

WHERE YOUR MONEY STORY BEGAN

Research on financial social work confirms that the money beliefs driving your current financial behavior were largely formed in childhood through your family’s financial socialization (Gudmunson & Danes, 2011).

You absorbed messages about money from:

- Your primary caregivers: What they said about money (directly and indirectly through their actions)

- Your relatives, mentors, and friends: The attitudes they modeled around spending, saving, and wealth

- Your early experiences: Whether money felt scarce or abundant, whether your needs were met, whether financial stress was present

These early lessons created what researchers call “money scripts,” unconscious beliefs that automatically guide your financial decisions as an adult (Klontz et al., 2011).

Then Came Social Work School

In graduate school and throughout your career, you absorbed additional money messages from social work culture:

- “If you cared about money, you wouldn’t be in this field”

- “Real helpers prioritize service over salary”

- “Financial struggle proves your commitment”

The result? Many social workers carry layered beliefs about money that work against their financial wellbeing, beliefs from childhood compounded by professional socialization that valorizes financial sacrifice.

THE IMPACT ON FINANCIAL WELLBEING

Financial wellbeing isn’t just about having money; it’s about having both:

- Security: Meeting current obligations, feeling financially secure

- Freedom: Having financial freedom of choice, being in control of your finances

(Consumer Financial Protection Bureau, 2015; Vlaev & Elliott, 2014)

When your relationship with money is rooted in shame, scarcity, or the belief that you don’t deserve financial stability, it’s nearly impossible to achieve either dimension of financial wellbeing.

But here’s the good news: once you understand where your money beliefs come from, you can choose which ones to keep and which ones to revise.

THE PATH FORWARD: EXPLORING AND REVISING YOUR MONEY STORY

The money beliefs social workers carry don’t have to be permanent. Financial social work offers a framework for change (Sherraden & Huang, 2019). This isn’t about becoming “better with money” in some generic sense; it’s about understanding your specific relationship with money and making intentional choices that align with your actual values.

Step 1: Explore Your Money Messages

Start by uncovering the money lessons you absorbed. These questions aren’t just intellectual exercises; they’re the foundation for understanding why you make the financial choices you do.

Think back to your childhood and early adulthood:

- What did your parents or caregivers say about money? Both directly (“Money doesn’t grow on trees”) and indirectly (Did they argue about money? Avoid talking about it? Display anxiety or confidence around finances?)

- What money messages did you pick up from other relatives, mentors, or friends?

- Was money scarce or abundant in your household? How did that shape your sense of security?

- Were your needs consistently met, or did you learn to downplay what you needed?

- What did you learn about people who had money? People who didn’t?

Then consider your professional socialization:

- What money messages did you absorb in social work school?

- How does your workplace culture talk about money, salaries, and financial security?

- What do you believe “good social workers” are supposed to think or feel about money?

Step 2: Assess Which Beliefs Serve You (and Which Don’t)

Look at the money beliefs you’ve identified. Some of them may be adaptive and helpful. Others may be holding you back.

For each belief, ask:

- Does this belief support my financial wellbeing?

- Does it help me make decisions aligned with my values?

- Or does it keep me stuck in patterns that don’t serve me?

Examples of beliefs to reconsider:

- “I should always put others’ needs first” → This might lead to chronic under-earning and difficulty setting boundaries around unpaid work.

- “Money isn’t that important” → This might prevent you from building savings or planning for the future.

- “Wanting financial security makes me selfish” → This might sabotage your ability to negotiate, save, or invest.

Step 3: Create Your Financial Vision

What does financial wellbeing look like for you—not society’s definition, not the field’s implicit expectations, but yours?

This vision becomes your North Star for making financial decisions aligned with your actual values.

Consider:

- What would it feel like to have financial security?

- What financial goals matter to you? (Emergency fund? Retirement savings? Paying off student loans? Being able to take a vacation without guilt?)

- What does “enough” look like for you?

- How would financial stability change your daily life? Your sense of safety? Your ability to do meaningful work?

Write it down. Be specific. This isn’t about becoming wealthy. It’s about defining what financial wellbeing means to you.

Step 4: Align Your Behaviors With Your Revised Beliefs

Once you’ve identified which money messages to keep and which to revise, you can begin making intentional choices about earning, spending, saving, and investing that reflect your genuine values rather than inherited scripts.

This is where the rubber meets the road. Start small:

- If you’ve been avoiding looking at your bank account: Set a time this week to review your finances with curiosity, not judgment.

- If you’ve been undercharging for your services: Research market rates and practice saying your new fee out loud.

- If you’ve been saying yes to unpaid work: Practice saying no to one thing this month. Notice what comes up.

- If you’ve been feeling guilty about spending on yourself: Identify one thing that would genuinely improve your wellbeing and give yourself permission to buy it.

Remember: sustainable change happens gradually. You’re not trying to fix everything at once. You’re building new neural pathways around money, one decision at a time.

Step 5: Expect Discomfort (and Keep Going Anyway)

When you start challenging old money beliefs, your nervous system may sound alarms:

- “This feels selfish”

- “I’m betraying my values”

- “Who am I to want financial security?”

This discomfort is not evidence that you’re doing something wrong. It’s evidence that you’re doing something different.

The goal isn’t to eliminate the discomfort; it’s to recognize it for what it is (old conditioning) and move forward anyway.

THE BOTH/AND, AGAIN

- You can value meaningful work AND build wealth.

- You can be committed to social justice AND have financial security.

- You can help others AND prioritize your own financial wellbeing.

Improving your relationship with money isn’t about abandoning your values; it’s about ensuring your financial behaviors actually support the life you want to live, both personally and professionally.

YOUR MONEY STORY REFLECTION

Use these questions to begin uncovering your money story:

About Your Childhood:

- What money beliefs, thoughts, and attitudes did you learn from your primary caregivers?

- What money messages did you absorb from relatives, mentors, and friends?

- How would you describe your childhood financial circumstances?

About Your Current Relationship With Money:

- Which childhood money lessons still impact your actions today?

- Which money beliefs do you find appropriate and relevant?

- Which money messages would you like to adjust to better fit who you are as an adult and the goals you want to achieve?

About Your Financial Vision:

- What does financial wellbeing look like for you specifically?

- What financial goals matter most to you right now?

- What’s one small financial behavior you could change this month that would align with your values?

What About the System?

f you’re reading this and thinking, “But what about the fact that social workers are systematically underpaid? Isn’t this just personal responsibility rhetoric that ignores structural problems?”

You’re right to question this. And it’s exactly what I’ll address in my next post.

The social worker pay gap is real, structural, and unjust. And many social workers carry internalized beliefs that prevent them from advocating for better compensation. Both are true. Both need attention.

In my next post, we’ll explore how personal work and systemic change must coexist, and why confusing the two keeps social workers stuck in both directions.

If you’d like support working through your money story in therapy…

Understanding your money story intellectually is one thing. Untangling the emotional charge around money, the shame, the anxiety, the worthiness wounds, often requires therapeutic support.

In my clinical practice, I work with social workers and other high-achieving professionals to:

- Identify and process the root experiences that shaped your relationship with money

- Untangle self-worth from financial circumstances

- Build capacity for self-advocacy without guilt

- Create sustainable financial patterns that align with your values

If you’re ready to do this work, I’d be honored to support you.

Learn more about working with me

Frequently Asked Questions About Money Beliefs Social Workers Develop

Where do money beliefs come from?

Understanding the money beliefs social workers develop is the first step toward changing them. Money beliefs are formed primarily through childhood financial socialization, what you learned from parents, caregivers, relatives, and early experiences with money. Research shows these unconscious beliefs, called “money scripts,” are absorbed before age 7 and continue to influence adult financial decisions. For social workers, these childhood messages are often reinforced by professional training that emphasizes self-sacrifice and the “helper” identity.

What are money scripts and how do they affect social workers?

Money scripts are unconscious beliefs about money that automatically guide financial decisions. Common money scripts social workers carry include “money isn’t that important,” “I should always put others first,” or “wanting financial security is selfish.” These scripts lead to specific behaviors like chronic undercharging, avoiding salary negotiations, or sabotaging financial stability, which directly impact your financial circumstances over time.

How does the Financial Social Work framework help change money beliefs?

Financial Social Work, developed by Reeta Wolfsohn and the Center for Financial Social Work, provides a framework for understanding how your relationship with money drives financial behavior, which in turn determines your financial circumstances. This approach helps you identify inherited money beliefs, assess which ones serve you, and create new patterns aligned with your actual values, addressing both psychological and practical dimensions of financial wellbeing.

What if my money beliefs come from trauma?

If your money beliefs are rooted in financial trauma, experiences like childhood poverty, sudden financial loss, or having basic needs unmet, they often carry more emotional intensity and are harder to change through education alone. Trauma-informed therapy approaches like EMDR can help process these memories and update the beliefs formed during traumatic experiences. The goal isn’t to erase what happened, but to separate the past experience from your current financial reality so you can make decisions based on present circumstances rather than old wounds.

Can therapy help with unhealthy money beliefs?

Yes. Trauma-informed therapy approaches like EMDR can help process the childhood experiences where problematic money beliefs were formed. Therapy addresses the emotional charge around money, the shame, anxiety, and worthiness wounds, while practical financial education addresses budgeting, saving, and investing. Both dimensions are typically needed for sustainable change in your relationship with money.

How do I know which money beliefs to keep and which to change?

Ask yourself: Does this belief support my financial wellbeing? Does it help me make decisions aligned with my values? Or does it keep me stuck in patterns that don’t serve me? For example, “I should be thoughtful about spending” might be helpful, while “spending on myself is selfish” likely isn’t. The key is distinguishing between beliefs that genuinely reflect your values versus beliefs you absorbed uncritically from childhood or social work culture.

How do social work schools contribute to unhealthy money beliefs?

Social work graduate programs often reinforce problematic money beliefs through explicit and implicit messaging. Many programs emphasize “passion over pay,” frame financial concerns as incompatible with social justice values, and rarely include financial literacy or salary negotiation training. Field placements are often unpaid or underpaid, normalizing financial sacrifice. The culture valorizes self-sacrifice while treating financial ambition as suspect. These messages compound whatever money beliefs students brought from childhood, creating a professional identity where wanting financial security feels like betraying the profession’s mission.

Can I change my financial circumstances without changing my money beliefs?

Short-term improvements are possible; you might get a raise, inherit money, or pay off debt. But if your underlying money beliefs haven’t changed, you’ll likely unconsciously recreate similar patterns. For example, if you believe “I don’t deserve financial ease,” you might get a higher-paying job but then take on unpaid work that keeps you stressed, or avoid building savings because it feels uncomfortable. Sustainable financial change requires addressing both practical circumstances (earning, budgeting, investing) AND the psychological patterns driving your financial behaviors.

What’s the connection between money beliefs and social work burnout?

Money beliefs directly impact burnout through the Relationship → Behavior → Circumstances chain. If you believe “good social workers sacrifice financially,” you’ll engage in behaviors like accepting low pay without negotiation, staying in underpaying jobs, or working multiple jobs to make ends meet. These financial circumstances create chronic stress that contributes to compassion fatigue, resentment, and ultimately burnout. Addressing money beliefs is essential for sustainable social work practice.

How long does it take to change money beliefs?

Changing money beliefs is a gradual process, not a quick fix. The timeline varies based on how deeply ingrained the beliefs are and whether they’re tied to trauma. Some people notice shifts in 3-6 months of intentional work (therapy, reflection, practicing new behaviors), while deeper patterns may take 1-2 years. The key is consistency, making small aligned decisions that reinforce new beliefs over time, rather than trying to change everything at once.

REFERENCES

Consumer Financial Protection Bureau. (2015). Financial well-being: The goal of financial education. Washington, DC: CFPB.

Gudmunson, C. G., & Danes, S. M. (2011). Family financial socialization: Theory and critical review. Journal of Family and Economic Issues, 32(4), 644-667.

Klontz, B., Britt, S. L., Mentzer, J., & Klontz, T. (2011). Money beliefs and financial behaviors: Development of the Klontz Money Script Inventory. Journal of Financial Therapy, 2(1), 1-22.

Sherraden, M. S., Frey, J. J., & Birkenmaier, J. (2016). Financial social work. In J. J. Xiao (Ed.), Handbook of consumer finance research (2nd ed., pp. 115-127). Springer.

Sherraden, M. S., & Huang, J. (2019). Financial social work. In Encyclopedia of Social Work. Oxford University Press. https://doi.org/10.1093/acrefore/9780199975839.013.923

Shim, S., Barber, B. L., Card, N. A., Xiao, J. J., & Serido, J. (2010). Financial socialization of first-year college students. Journal of Youth and Adolescence, 39(12), 1457-1470.

Stuart, P. H. (2016). Financial capability in early social work practice: Lessons for today. Social Work, 61(4), 297-304.

Vlaev, I., & Elliott, A. (2014). Financial well-being components. Social Indicators Research, 118(3), 1103-1123.

Webley, P., & Nyhus, E. K. (2006). Parents’ influence on children’s future orientation and saving. Journal of Economic Psychology, 27(1), 140-164.

Wolfsohn, R., & Michaeli, D. (2014). Financial social work. Encyclopedia of Social Work. National Association of Social Workers and Oxford University Press.

About the author:

Dorlee Michaeli, MBA, LCSW, specializes in EMDR therapy for high-achieving professionals struggling with imposter syndrome. She provides consultation for complex cases involving perfectionism and workplace anxiety. Learn more.

{kind=link}

Hi Dorlee. There are some good nuggets in this article.

-“Money scripts are absorbed before age 7 per research”

– Financial wellbeing is security and freedom

-And I love anything that is both/and, because life is too complex for reductionist theories, even about money.

One thing I haven’t seen noted is how religious beliefs can also impact money beliefs. Not only was I raised to think that volunteering is a noble cause (and thus sacrifice of money for the service of others), but I was taught money is the root of all evil. A rich man cannot get to heaven. Etc etc. This is constantly preached in so many settings. I wonder what other religious teachings or spiritual beliefs might also drive this narrative?

Thank you for adding this, Randi. It is such an important dimension. Religious and spiritual teachings can profoundly shape our early money narratives, especially when service, sacrifice, and morality become intertwined with earning. I appreciate you naming how these messages can linger internally long after the context changes.

Dorlee,

How wonderful that you are creating space for this important conversation and work.

Having dedicated the past 29 years of my life to creating Financial Social Work for clients and social workers, I know, as you do, Financial Healing is Holistic Healing – it is social work in action!

Without it, our colleagues and clients aren’t receiving the most complete care.

Reeta, I’m so grateful for your encouragement and for the trailblazing work you’ve done over the past three decades. Financial Social Work has transformed how many of us understand healing and sustainability in our profession. Your leadership continues to inspire my work and so many others.